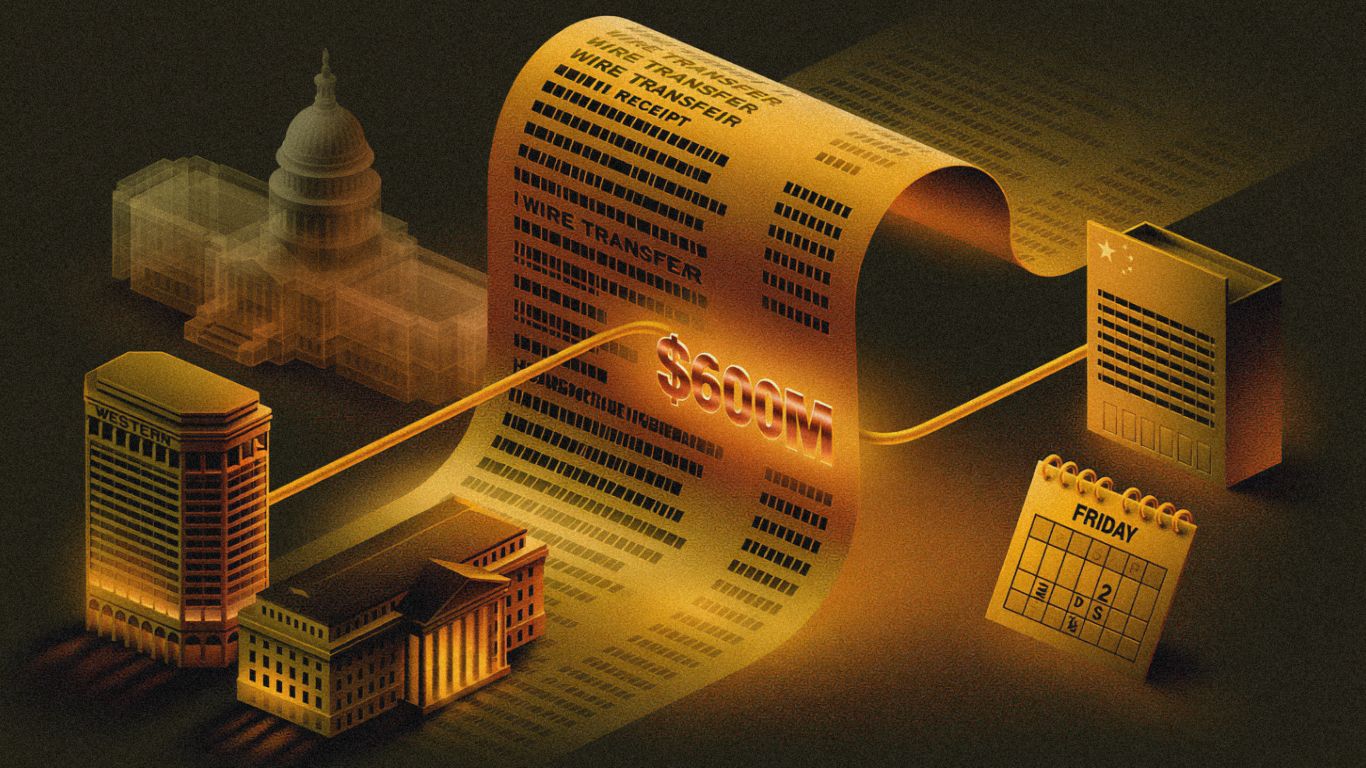

Yesterday we said to watch what companies do rather than what they say about China, and pointed to AstraZeneca as the tell. Today AstraZeneca made the point louder than we could have.

The company is paying $600 million upfront for global rights to Zegfrovy, an EGFR inhibitor for lung cancer, from China’s Dizal Pharmaceutical. That is the biggest upfront of AstraZeneca’s entire China run and its fifth licensing deal with a Chinese drugmaker since the start of 2025. It lands three days before Merck, AbbVie, Lilly, Pfizer, and BMS have to explain their China trials to the House Select Committee.

If you needed a single data point to capture how the pharmaceutical industry actually feels about the congressional probe, this is it.

Zegfrovy is not a cheap option on early science. It is already approved in both the United States and China for a form of advanced non small cell lung cancer with specific mutations, and it is under regulatory review as a first line therapy. AstraZeneca said it fits alongside its existing EGFR lung cancer franchise, which is one of the strongest in the industry. When a company pays $600 million upfront for an approved drug that slots directly into a category it already dominates, it is expressing conviction, not hedging.

The FDA approved injectable Leqembi, continuing the pattern of post Makary reversals. Pfizer reshuffled its obesity leadership after years of coming up short. And the July 17 deadline is now two days away.

AstraZeneca’s $600M Upfront Is the Loudest China Signal of the Year

What Happened: AstraZeneca agreed to pay $600 million upfront for global rights to Zegfrovy from Dizal Pharmaceutical of China, according to STAT. The drug is an EGFR inhibitor already approved in both the U.S. and China for advanced NSCLC with certain mutations and under review as a first line therapy.

Why This Deal Is Different from the Rest

We have tracked a lot of China deals this year. BMS/Hengrui ($15.2 billion). Pfizer/Innovent ($10.5 billion). Lilly/Haisco ($3 billion plus). BioNTech/DualityBio ($1 billion). AstraZeneca/CSPC ($1.77 billion). Most of these share a common structure: modest upfront payment, large milestones that only come due if the drug works, and assets that are clinical stage rather than approved. That structure lets a buyer take a position in Chinese science while limiting the cash at risk if the program fails.

The Zegfrovy deal breaks that pattern. $600 million upfront is real money. The drug is already on the market. It has regulatory approval in two major jurisdictions. It is under review for a first line label expansion that would dramatically increase the patient population. AstraZeneca is not buying an option on unproven science. It is buying a commercial asset at a price that reflects proven clinical value.

The Timing Is the Statement

AstraZeneca is not among the five companies named in the House Select Committee probe, which gives it operational freedom the named five do not have right now. But the timing of this announcement—three days before the July 17 deadline, in the same month that the Biotech Investment National Security Act sits pending in Congress—is the most unambiguous signal we have seen from any company about how the industry reads the political risk.

A company genuinely worried about legislative restrictions on China licensing would have delayed this announcement. It would have structured the deal to minimize China exposure, or at least avoided putting a $600 million China upfront in the news cycle during the week the probe reaches its climax. AstraZeneca did none of that. It wrote its biggest upfront check to a Chinese partner and put its name on the press release.

This is AstraZeneca’s fifth China licensing deal since the start of 2025. Three with CSPC (obesity, chronic disease, kidney disease worth up to $1.77 billion). One with Sino Biopharmaceutical (inhaled respiratory). And now Dizal at $600 million upfront. Only Roche has been more active among major pharma companies. The cadence has not slowed despite the probe. If anything, it has accelerated.

The Akero/Fairmount Startup Tells the Same Story at a Different Scale

The same pattern showed up a layer down this week. The former executive team of Akero Therapeutics, recently sold to Novo Nordisk, partnered with the prolific company creator Fairmount to launch a new public biotech built around a long acting immunology drug licensed from a Chinese firm. Western talent, Western capital, Chinese molecule. It is the same engine driving the AstraZeneca deal, just at startup scale.

When both the largest pharma companies and the newest biotech startups are sourcing their lead assets from Chinese partners in the same week, the pattern is systemic. This is not one company making an unusual bet. This is the industry’s operating model, and it is running at full speed regardless of what Washington is doing.

Our Pro brief analyzes why the size and timing of the Zegfrovy deal matter more than the number of deals, and what it tells you about how the industry prices political risk. [Details below.]

Injectable Leqembi Gets Cleared, and the FDA Keeps Reversing in Companies’ Favor

What Happened: The FDA approved a subcutaneous injectable version of Leqembi (lecanemab), the Eisai and Biogen Alzheimer’s antibody. STAT framed it as another post Makary reversal.

Why the Formulation Change Matters

Leqembi until now required regular intravenous infusions, which meant patients had to travel to an infusion center, sit for an extended session, and be monitored for infusion related reactions. For Alzheimer’s patients, many of whom have cognitive impairment, rely on caregivers for transportation, and already face a heavy burden of medical appointments, the infusion requirement was a genuine barrier to uptake. Biogen has acknowledged that Leqembi’s launch has been slower than expected, and the formulation burden was one of the reasons.

A subcutaneous injection—essentially an at home shot similar to how patients take insulin or GLP 1 drugs—removes the infusion requirement. Patients or caregivers can administer the drug without traveling to a clinic. The convenience improvement is the kind of change that can meaningfully expand uptake for a drug whose clinical benefit has been demonstrated but whose practical barriers have limited adoption.

The FDA Reversal Pattern Continues

STAT calling this “another post Makary reversal” fits the pattern we have tracked since the spring. Under acting leadership, the FDA has been consistently more willing to approve, expand, and reverse previous restrictive positions than it was during the Makary and Prasad era.

The sequence is now long enough to call it a trend rather than a series of coincidences. The FDA reversed its demand for additional data on UniQure’s Huntington’s gene therapy and accepted the filing for accelerated approval. It accepted Replimune’s RP1 BLA after two prior rejections. REGENXBIO is filing its Duchenne gene therapy expecting a friendlier reception. Casgevy was expanded into younger children through CNPV. And now injectable Leqembi is approved, removing a barrier that the previous administration may have been slower to address.

The practical implication for the industry: companies with programs that stalled or were delayed over the past 18 months should be evaluating whether the current regulatory environment favors resubmission. The window is open. Whether it stays open depends entirely on who the administration eventually nominates as permanent commissioner. Acting leadership is temporary by definition, and a new permanent appointee with a different regulatory philosophy could shift the posture again.

Agenus Cuts Its Losses to Bet on the Hardest Target in Immunotherapy

What Happened: Agenus discontinued its Phase 3 trial in metastatic colorectal cancer to concentrate resources on MSS colon cancer, one of the most stubbornly immunotherapy resistant settings in oncology.

Why This Matters: MSS (microsatellite stable) colon cancer has defeated essentially every checkpoint inhibitor and immunotherapy combination thrown at it. Unlike MSI high (microsatellite instability high) colon cancer, where Merck’s Keytruda has shown dramatic benefit, MSS tumors lack the high mutation burden that makes them visible to the immune system. The result: immunotherapy works beautifully in about 15% of colorectal cancers (MSI high) and barely works at all in the other 85% (MSS).

Agenus concentrating its shrinking resource base on the 85% is a high risk, high reward bet. If the company can show immunotherapy activity in MSS colon cancer—even modest activity—it would be cracking one of the most resistant problems in the field. The potential patient population is enormous because most colorectal cancer is MSS. But the history of failed attempts in this space is long, and a cash constrained biotech choosing to fight on the hardest possible battlefield is either visionary or a misallocation of its final resources. The data will tell.

The decision reflects the broader pattern of hard prioritization we have seen across the sector this year. enGene halved its workforce. Neumora cut 35% and then lost its lead drug. BioCryst closed its entire discovery center. Companies across biotech are choosing one shot on goal rather than spreading thin, and Agenus just chose the most difficult target available.

Pfizer Reshuffled Obesity Leadership After Years of Missing the Market

What Happened: Pfizer named Danna Breen vice president and head of obesity discovery following the departure of longtime scientific leader Kendra Bence.

The Gap Pfizer Needs to Close

Obesity is the biggest commercial opportunity in the pharmaceutical industry. Lilly has Foundayo approved, Zepbound growing, and retatrutide with two pivotal wins heading toward a 2027 launch. Novo has oral and injectable Wegovy across obesity, diabetes, and now MASH. The Medicare Bridge launched July 1 with both companies’ products covered at $50 per month. Retatrutide’s 28.3% weight loss matches bariatric surgery results.

Pfizer has almost entirely missed this. The company’s oral GLP 1 program, centered on danuglipron, repeatedly stumbled with tolerability and dosing problems that forced it to abandon or retool candidates while the incumbents extended their leads. Every quarter Pfizer spent struggling, Lilly and Novo were building manufacturing capacity, accumulating clinical data, establishing physician relationships, and securing payer coverage. The gap is not just one drug behind. It is an entire platform behind.

A new discovery head signals Pfizer is not conceding the category, but rebuilding an obesity pipeline from a standing start in 2026 is a daunting proposition. Discovery takes years. Clinical development takes more years. By the time a new Pfizer obesity candidate reaches Phase 3, retatrutide will have been on the market for years, and the next generation of competitors (amylin combinations, muscle preserving agents, novel oral mechanisms) will be well advanced.

The faster route to relevance would be acquisition. Pfizer has the balance sheet, the commercial infrastructure, and the strategic urgency to buy its way into the obesity market rather than waiting for internal discovery to produce a competitive candidate. Whether the next move in obesity from Pfizer comes from the lab or from the business development team will tell you how seriously the company assesses its own internal capability gap.

Strategic Themes

1. AstraZeneca’s $600M Upfront Settles the Question of How the Industry Reads the China Probe

Not an option bet. Not a milestone heavy hedge. $600 million in cash for an approved drug, announced three days before the congressional deadline, from a company that has now signed five Chinese deals since the start of 2025. The industry is not retreating. It is not pausing. It is paying full price for de risked Chinese assets at the moment of maximum political heat. The probe is a cost to be managed. The science is the reason to pay.

2. The FDA Under Acting Leadership Is Systematically Friendlier Than It Was Under Makary

UniQure reversed. Replimune accepted. REGENXBIO filing. Casgevy expanded. Injectable Leqembi approved. The pattern is consistent enough to act on. Companies with stalled or rejected programs should be evaluating resubmission. The window exists because acting leadership is temporary, and a permanent commissioner could change the posture. Moving now, while the regulatory environment favors approval, is the tactical play.

3. Pfizer Missing Obesity Is One of the Costliest Strategic Gaps of the Decade

The market that will exceed $100 billion in annual sales. The three tier portfolio (Foundayo, Zepbound, retatrutide) that Lilly built while Pfizer struggled with danuglipron. The Medicare Bridge that opened 60 million beneficiaries. Every month that passes without a competitive Pfizer obesity product widens the gap. A leadership change in discovery is necessary but not sufficient. The question is whether Pfizer acts through its checkbook or its lab—and how much time it has before the window closes entirely.

4. Friday Is Two Days Away, and the Industry Already Answered

The formal deadline is July 17. The formal responses will be carefully worded. But the industry’s real answer came this week in the form of $600 million wired to a Chinese company, a startup built around a Chinese molecule, and a pipeline of positive clinical readouts from Chinese licensed assets. Washington wants to know why pharma is in China. The answer is on every data slide at every medical conference this year: the science is too good to leave on the table.

Frequently Asked Questions

What is the AstraZeneca/Dizal deal?

$600 million upfront for global rights to Zegfrovy, an EGFR lung cancer drug already approved in both the U.S. and China and under review as a first line therapy. AstraZeneca’s fifth Chinese licensing deal since the start of 2025 and its biggest upfront. Announced three days before the July 17 congressional deadline.

What is the FDA reversal pattern?

Under acting leadership, the FDA has reversed several restrictive decisions from the Makary era. UniQure Huntington’s filing accepted. Replimune RP1 accepted after two CRLs. Casgevy expanded to younger children. Now injectable Leqembi approved. STAT called the Leqembi decision “another post Makary reversal.”

What happened with Agenus?

Dropped its Phase 3 in metastatic colorectal cancer to concentrate on MSS colon cancer, one of the most immunotherapy resistant settings. High risk bet on the 85% of colorectal cancers where checkpoint inhibitors have historically failed.

Why did Pfizer change its obesity leadership?

Named Danna Breen as VP and head of obesity discovery after Kendra Bence departed. Pfizer’s oral GLP 1 program (danuglipron) repeatedly stumbled while Lilly and Novo built dominant franchises. Rebuilding from a standing start while competitors are years ahead is the strategic challenge.

What is the Akero/Fairmount startup?

Former Akero Therapeutics executives (company sold to Novo Nordisk) partnered with Fairmount to launch a new public biotech around a long acting immunology drug licensed from a Chinese firm. Western talent and capital, Chinese molecule.

When is the China probe deadline?

Friday, July 17. Two days from today. Merck, AbbVie, Lilly, Pfizer, and BMS must respond.

BioMed Nexus Pro — What Institutional Subscribers Are Reading Today

AstraZeneca’s $600M Is the Cleanest Signal Yet. We analyze why the size and timing of the Zegfrovy deal matter more than the deal count, what it tells you about how the industry prices political risk in real time, and what to watch from the five named companies in the two weeks after Friday.

The FDA Reversal Pattern Is Tradeable. We identify which pending FDA decisions are most likely to break in companies’ favor under the current acting leadership, assess how long the window stays open, and evaluate the risk that a permanent commissioner appointment changes the posture.

Can Pfizer Rebuild Obesity From Behind? We assess whether a discovery leadership change can close a gap this wide, lay out why the faster route is acquisition rather than internal development, and identify which assets or companies Pfizer should be targeting.

Plus: Agenus MSS colon cancer bet, Akero/Fairmount Chinese licensing startup, injectable Leqembi uptake implications, Section 232 tariff countdown (16 days), and the full H2 catalyst calendar.

About BioMed Nexus

BioMed Nexus delivers institutional grade intelligence to biotech and pharma executives, investors, and clinicians. Our daily briefings and deep dive analyses cut through the noise to deliver the strategic insights that drive better decision making in the life sciences.

Subscribe to receive daily updates and gain access to BioMed Nexus Pro institutional intelligence briefs.